Portfolio update & stock comments 10-Feb-21

watch that inflation closely

As at 9th-Feb-2021, the portfolio is up 57% YTD in just a little over a month, mainly contributed by: $FUTU +238%, $APPS +63%, $BIDU +36%, $SE +38%, $TECHY +36%, $TDIC+44%.

Please visit deepyield.io for more details.

This is not normal and cannot be repeated. The market does seem to reach a peak of FOMO and complacency.

We would suggest readers to start to accumulate protective trades, such as index ETF puts, Volatility ETF calls and long-end Treasury short as we suggested at the beginning of the year, but to avoid outright short high beta names. (for that reason, we’ve closed out our $F short position and took some loss)

$SHOP Payment on Facebook

Shortly after we closed out $SHOP position to fund other names, $SHOP rallied ~7% on the news that Shopify will start to provide Shopify Payment on Facebook & Instagram.

In our newsletter about $SHOP, we already modelled that Shopify Payment will be the strongest growth segment out of all Shopify Merchant solutions, and grow its own revenue from 1.4billion in 2020 to 3.8billion in 2025, and contribute over 30% of total Shopify 2025 revenue. However as we explained, payments will become a highly commoditized sector and profit margin will turn lower. More importantly, as we like $SHOP’s bright future, its current expensive valuation might require long term patience and some potential opportunity costs vs. investing in other growth names.

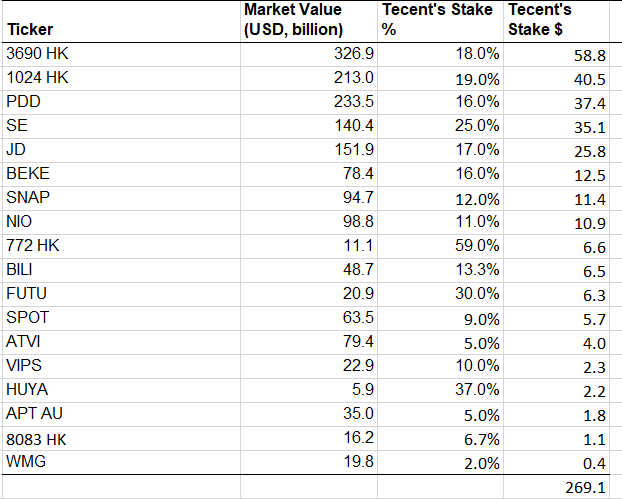

Kuaishou IPO ($1024 HK) and update on Tencent public investment book

In this newsletter, we explained why we see Tencent as the digital version of Berkshire Hathaway. One of its private unicorn Kuaishou just recently IPO’d in Hong Kong Exchange. Kuaishou, in one sentence, is the Tiktok for lower tier cities in China, with very strong e-Commerce potential. The close price on 10-Feb-2021 puts Kuaishou at a valuation of 1.65 trillion HKD or 213 billion USD, an $150 billion mark-up from our previous conservative assumption of $60 billion USD in its private book.

Let’s take this chance to refresh Tencent’s public investment book.

Our estimates in the below table shows Tencent is now managing a $270 billion USD public market portfolio, almost 30% of its own market cap. Adding its private investments, we think Tencent’s total investment book might be close to 40% of its total worth, further substantiating our “Berkshire Hathaway” view.

This increases both Tencent’s market beta (esp. to Asian growth) and attractiveness of its core business at the same time.

Watch out inflation !!

The real reason to cause us to have a more cautious view, is the ongoing hot expectation of inflation.

Below is a very interesting chart. The 5y breakeven rate (orange) is basically the market expectation of the average annualised inflation rate from 2021 to 2025. The 5y forward 5y breakeven rate (green) is basically that expectation but for the period 2026 to 2030. It curiously shows the expectation of the front end inflation has quietly shot over above that of the back end.

Quicker the inflation upside surprise comes, the earlier FED might respond to start the tightening cycle. As the market has always been trying to front run FED, any leading indicators for stronger CPI or PCE should be your alerts to prepare dialing down risk exposure.

Last but not leastly, this Stan Druckenmiller interview is just as good as always.

Hope you can learn a thing or two as we do from it.

https://www.goldmansachs.com/insights/talks-at-gs/stanley-druckenmiller.html